Shaking Hands With Himself?

Trump’s $1.776 Billion Pardon Fund, the IRS Deal That Isn’t a Deal, and What a Future Administration Can Do About It

DULY CONSIDER · LAW · ACCOUNTABILITY · THE RECEIPTS

IRS · DOJ · $1.776 BILLION · THE SETTLEMENT THAT ISN’T ONE

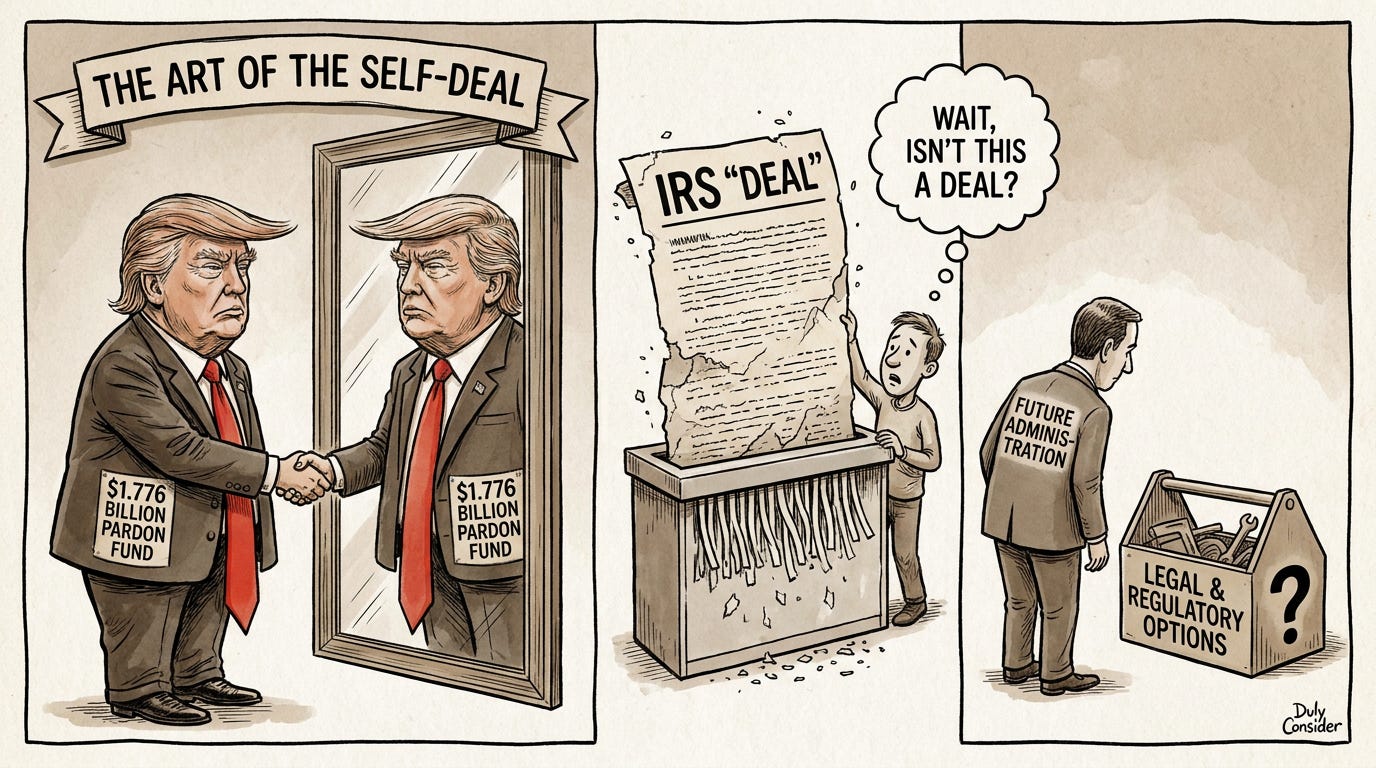

A sitting president sued a government agency he controls, settled with himself, directed $1.776 billion in taxpayer funds to his pardoned allies, waived his own IRS audit as a term of the deal, and called it justice. In 250 years of American history, nothing like this has happened. Here is the legal record a future administration will need.

On May 18, 2026, the Department of Justice announced the creation of a $1.776 billion fund — the amount chosen, the DOJ noted, in honor of the nation’s founding year — to compensate individuals who allege they were unfairly targeted by the Biden administration.1 The fund’s creation was the price of Donald Trump dropping his $10 billion lawsuit against the Internal Revenue Service. As part of the same settlement, the IRS agreed to issue a public apology to the president and to waive an outstanding audit of his personal finances.2 The commission overseeing distribution has broad authority and few constraints on who can claim.

Senate Minority Leader Chuck Schumer called it precisely what it is: “Trump is shaking hands with himself in order to fund his insurrectionist army to the tune of billions.”1 That framing is not hyperbole. It is a legal description of what occurred. A president negotiated a settlement with a government agency he controls, on terms that benefit him personally, his business interests, and the political allies he pardoned. The adverse party in the settlement is the same person as the benefiting party. That is the definition of self-dealing.

This piece documents the four specific legal problems with the fund, the historical record that establishes its unprecedented nature, and the legal arguments a future administration needs already in the record.

PROBLEM ONE

The Settlement That Isn’t One

A valid settlement requires adverse parties. These aren’t.

THE SELF-DEALING STRUCTURE · DOCUMENTED · SOURCE: DOJ PRESS RELEASE, ABC NEWS, CNN, MAY 18, 2026

A settlement is a legal instrument that resolves a dispute between adverse parties — parties with genuinely opposing interests, each making concessions to avoid the cost and uncertainty of litigation. The settlement derives its legal validity from the adversarial nature of the negotiation. When one party controls both sides, the adversarial requirement is absent and the instrument is not a settlement. It is a directed payment dressed in settlement clothing.

Trump, as president, controls the DOJ. The DOJ controls the IRS’s litigation posture. Trump, as plaintiff, sued the IRS for $10 billion. Trump, through the DOJ, settled that lawsuit on terms that include a taxpayer-funded compensation pool available to his allies, a public apology from the IRS to him personally, and the waiver of an audit that would examine his own finances.2 The plaintiff and the settling defendant are the same person exercising authority through different institutional channels.

Legal experts described the original lawsuit as “unprecedented” — a sitting president suing a government agency he commands.3 The settlement is more unprecedented still. No prior administration has resolved a president’s personal lawsuit against his own government by directing taxpayer funds to his political allies and waiving his personal tax obligations.

The teller at gunpoint in this bank robbery, complies. Documents the duress. Preserves the challenge for when the gun is no longer at the window. That is what this piece is: the documented record.

PROBLEM TWO

A Pardon Is Not an Exoneration

The Supreme Court said so. The fund treats it as one anyway.

PARDON IS NOT EXONERATION · SUPREME COURT ON THE RECORD · NIXON V. UNITED STATES (1993)

The January 6th participants who are eligible to claim from the fund were charged with federal crimes, tried before independent federal juries, convicted on the evidence presented, and sentenced by independent federal judges. President Trump pardoned approximately 1,500 of them on his first day in office.4 The pardons are legally defensible as an exercise of the pardon power. They are also, legally, not what the fund treats them as.

The Supreme Court stated in Nixon v. United States (1993) that a pardon “is in no sense an overturning of a judgment of conviction by some other tribunal; it is an executive action that mitigates or sets aside punishment for a crime.”5 The conviction stands. The prosecution was lawful. The pardon removes the punishment — it does not retroactively establish that the prosecution was wrongful, that the government caused harm, or that the convicted are owed compensation.

The fund’s framework — providing a mechanism for pardoned January 6th participants to claim taxpayer compensation for “government overreach” and to receive “formal apologies” from the government — treats the pardon as an exoneration the Supreme Court explicitly says it is not. The three conclusions the fund requires — the prosecution was wrongful, the government caused harm, and the pardoned are owed compensation — are each separate legal determinations that require separate legal authority. The pardon provides none of them. The president does not have unilateral authority to make any of them.

PROBLEM THREE

No Historical Precedent

The only comparison that exists is structurally the opposite.

NO HISTORICAL PRECEDENT · THE ONLY COMPARISON INVERTS THE ARGUMENT

The closest historical comparison to a government compensation fund following a mass pardon is the Civil Liberties Act of 1988, in which Congress apologized to Japanese Americans interned during World War II and created a $1.25 billion compensation fund.6 The DOJ has modeled the new fund’s structure on similar victim compensation frameworks.

The comparison is precisely backwards. The Japanese Americans interned during World War II were never charged with crimes. They were never tried. They were never convicted. They were innocent civilians imprisoned without due process, without individualized hearings, on the basis of ethnicity alone. The government compensated genuine victims of genuine government wrongdoing — people against whom the legal system was deployed without legal justification.

The January 6th participants received the full process of American criminal law: indictment, trial, jury deliberation, conviction on evidence, sentencing by an independent judiciary. The process worked as designed. The outcomes were legally sound. The pardon that followed was an executive act of mercy, not a finding of innocence. Compensating them from public funds as though they were the Japanese American internees is not an analogy. It is an inversion.

In 250 years of American history, no administration has created a taxpayer-funded compensation mechanism for people who were convicted of crimes, sentenced, and then pardoned. The pardons are legally defensible. The compensation fund that follows them has no precedent and no legal foundation.

PROBLEM FOUR

The Audit Waiver

A president cannot direct the IRS to drop his own audit as a term of his own settlement.

As part of the settlement, the IRS agreed to waive an outstanding audit of Donald Trump’s personal finances.2 This element of the deal is the most direct and least ambiguous abuse of authority in the entire arrangement.

The IRS conducts audits under statutory authority established by Congress. The president does not have authority to direct the IRS to abandon an audit of himself as a term of a settlement he negotiated with himself. The conflict of interest is not structural or abstract. It is personal and financial. The person who benefits from the audit waiver is the same person who directed the DOJ to accept the settlement terms that included it.

A future Treasury secretary can rescind the audit waiver. It was accepted under conditions that vitiate its validity — an adverse party cannot waive a legal obligation owed to the public on behalf of the public when that adverse party is the same person who benefits from the waiver. The statutory authority to conduct audits belongs to the IRS under the Internal Revenue Code. It cannot be surrendered by executive settlement.

THE RECORD

What a Future Administration Has

The legal arguments that must be built into the record now.

WHAT A FUTURE ADMINISTRATION HAS · THE LEGAL RECORD BEING BUILT NOW

The appropriate political response to a settlement made under duress — a president with institutional control of every party to the negotiation, acting in his own financial and political interest — is to comply while documenting, to preserve the challenge for when the institutional constraints are restored, and to build the legal record now that a future administration will need to act.

Congress has oversight authority over executive branch fund disbursements. The Joint Committee on Taxation has oversight over large IRS settlements. The Treasury Inspector General for Tax Administration can examine whether the audit waiver followed proper procedure. Democratic members of Congress have already introduced legislation to bar January 6th defendants from receiving compensation from the fund.1 Each of these actions builds the record.

The fund closes December 15, 2028 — one month before Trump’s term ends.1 The timing is not coincidental. A future administration taking office in January 2029 inherits whatever distributions have been made and whatever legal record has been built against them. The work of building that record is now.

The settlement is not valid. The audit waiver is not valid. The compensation of pardoned insurrectionists as victims of their own lawful prosecution has no legal foundation and no historical precedent. The teller complies under duress. Documents everything. And waits for the next administration to do what this one prevented.

REFERENCES

1

2

3

4

POLITIFACT / WIKIPEDIA (JANUARY 20, 2025) Trump pardons January 6 defendants — Presidential Proclamation 10887, January 20, 2025; approximately 1,500 pardons and commutations; Proud Boys leader Tarrio released; seditious conspiracy convictions vacated

5

SUPREME COURT OF THE UNITED STATES (1993) Nixon v. United States, 506 U.S. 224 (1993) — pardon “is in no sense an overturning of a judgment of conviction by some other tribunal; it is an executive action that mitigates or sets aside punishment for a crime”; conviction stands; prosecution remains lawful

6

WAKE FOREST LAW REVIEW / CIVIL LIBERTIES ACT 1988 Civil Liberties Act 1988 — US government apologized to Japanese American internees and created $1.25 billion compensation fund; those individuals were never charged, tried, or convicted; innocent civilians imprisoned without due process; structurally opposite to compensation for convicted-then-pardoned individuals

7

NBC NEWS / CNBC (MAY 18, 2026) DOJ sets up $1.8B anti-weaponization fund — fund gives Jan. 6 rioters mechanism to seek taxpayer payouts; can issue formal apologies; acting AG Todd Blanche statement; Trump also withdrew administrative claims related to Mar-a-Lago raid and Russia investigation